Why Tracking Scope 3 Emissions is Non-Negotiable

Scope 3 emissions (indirect emissions across the value chain) typically account for 70–90% of a company's total carbon footprint. Ignoring them means reporting on a small fraction of actual impact. Tracking them is no longer optional under CSRD.

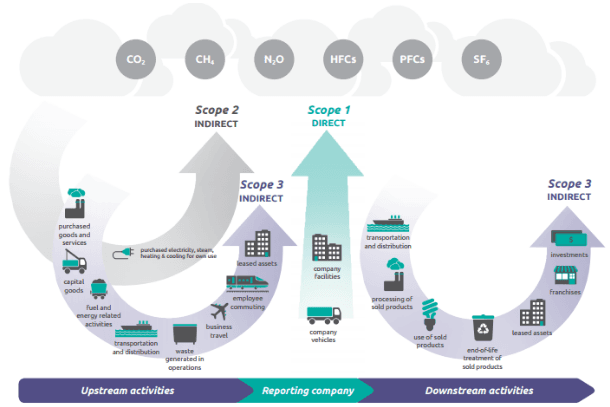

Source: GHG Protocol — You too can master value chain emissions

What Scope 3 covers

The GHG Protocol defines 15 categories of Scope 3 emissions, split between upstream and downstream activities. Upstream categories include purchased goods and services, capital goods, fuel and energy-related activities, upstream transport, waste, business travel, and employee commuting. Downstream categories include distribution, use of sold products, end-of-life treatment, leased assets, franchises, and investments.

For most companies, the largest categories are purchased goods and services (Category 1) and use of sold products (Category 11). The distribution varies significantly by sector, which is why a materiality-based approach to Scope 3 is essential before committing to full data collection across all 15 categories.

Why it cannot be avoided

The data challenge and how to handle it

Scope 3 data collection is genuinely difficult. Primary data (activity data directly from suppliers) is the gold standard, but it is rarely available at scale in the first reporting cycle. Spend-based estimation using economic input-output models provides a starting point, but with high uncertainty. Hybrid approaches, combining primary data for material categories with secondary data elsewhere, are standard practice.

The GHG Protocol Scope 3 Standard requires companies to document data sources, estimation methods, and uncertainty levels for each category. A gap analysis identifying where primary data is missing and what the uncertainty implications are is typically the first deliverable in a Scope 3 programme, and the most useful for prioritising supplier engagement.

Start with your Scope 3 baseline.

Acrypt delivers GHG Protocol-aligned Scope 3 inventories: primary data where available, documented assumptions where not, and a clear gap analysis.

Book a free consultation