ESG Reporting Frameworks: Which One Should You Use?

The ESG reporting landscape has multiple frameworks: GRI, ISSB, CSRD/ESRS, SASB, TCFD, CDP. They share similar objectives but serve different audiences and carry different obligations. Choosing the right one depends on your jurisdiction, stakeholders, and what you are trying to demonstrate.

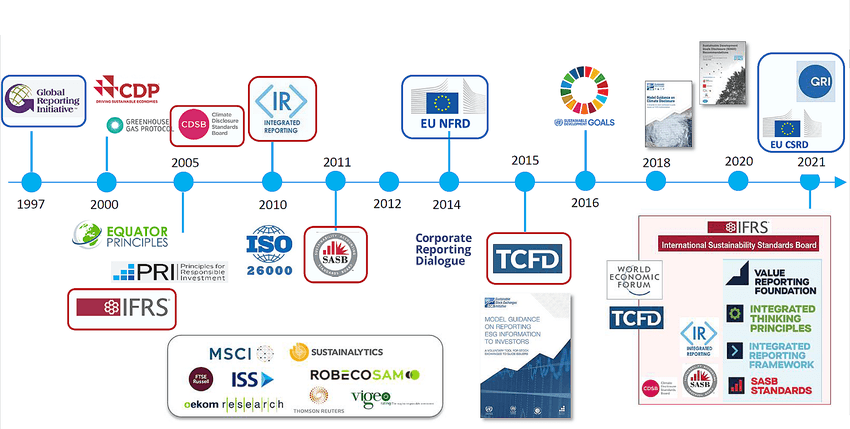

ESG reporting frameworks timeline. Source: Johannesburg Stock Exchange (2021)

The main frameworks compared

Double materiality: impact on the world AND financial risk. Mandatory for large EU companies from 2025, mid-sized from 2026. The most comprehensive and legally binding framework for European companies.

Impact materiality: how the organisation affects the environment and society. Widely used for voluntary sustainability reporting. Strong on stakeholder transparency.

Financial materiality: sustainability risks and opportunities relevant to investors. Climate disclosure under IFRS S2 is being adopted by capital markets regulators globally.

Financial materiality, sector-specific metrics. Useful for investor-focused reporting and as a supplement to broader frameworks. Now integrated into IFRS Foundation.

Governance, strategy, risk management, and metrics/targets for climate-related financial risks. Widely adopted and increasingly embedded in regulatory requirements.

Questionnaire-based disclosure on climate, water, and forests. Scores are used by buyers and investors. Increasingly required by procurement teams.

How to choose

For EU-headquartered companies or subsidiaries of EU groups, CSRD/ESRS is the starting point. It is a legal requirement, not a choice. The double materiality assessment required by ESRS can then be mapped to GRI and TCFD disclosures with relatively little additional effort, since the underlying data overlaps significantly.

For companies outside the EU, or those reporting voluntarily ahead of regulation, the choice depends on your primary audience. If your stakeholders are investors, ISSB/IFRS S1&S2 is the relevant standard. If your primary audience is procurement teams, CDP disclosure alongside Scope 3 data is more useful. If you are reporting for a broad stakeholder audience, GRI provides the most comprehensive coverage.

The practical reality is that most organisations operating across multiple stakeholder groups will use more than one framework. The key is to build a single, well-structured data collection process that feeds multiple reporting outputs, rather than running separate programmes for each framework.

Not sure which framework applies to you?

Acrypt can map your reporting obligations, identify which frameworks apply, and design a data collection process that satisfies all of them efficiently.

Book a free consultation